5 Steps to Year-End Retirement Plan Housekeeping

Ready or not here it comes. YEAR END. I know, I know. Your list is long and your time is short. But, it’s time for your retirement planning yearend check up. There are a few things all plan sponsors should think about as part of their end of the year work. It’s important for you and your employees to have the resources to retire, so you have a few housekeeping items to attend to. Not to worry, I’ll break down the big ticket items for you here.

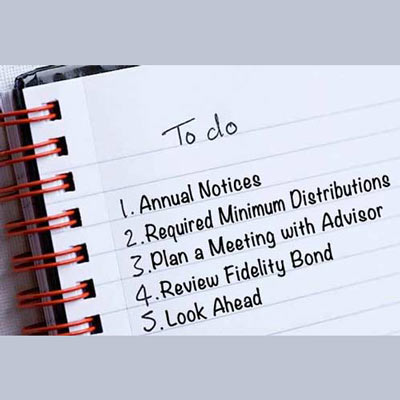

Year-End Retirement Plan Housekeeping List

Send out the proper annual notices.

There are several instances that require that you send an annual notice. If you have any of the following, you should check in with your TPA for assistance on sending out the proper annual notice to your employees.

Safe Harbor Plan – A safe harbor 401(k) plan requires the employer to provide timely notice to eligible employees informing them of their rights and obligations under the plan, and certain minimum benefits to eligible employees either in the form of matching or nonelective contributions.

Auto-Enroll or Auto-Increase Plan – If your plan uses automatic enrollment or automatic contribution increases, the IRS requires you to notify all employees who are eligible for the plan between 30 and 90 days prior to the beginning of each plan year. Talk with your TPA for exact requirements of your particular plan.

Qualified Default Investment Alternative (QDIA) – There is often confusion around the notice requirements for these plans. IRS regulations state that defaulted participants and beneficiaries (both active and terminated) who have failed to direct their investments should receive a notice. Your TPA is up to speed on the regulations surrounding these plans, please don’t hesitate to contact them for support. Operators are standing by!

Take Required Minimum Distributions (RMD).

For those staff members age 70.5 or older, it’s vital to ensure they are aware of the requirements for taking a distribution from their account. Timing is especially important in this case because there are deadlines and penalties associated with missing them. Traditional IRAs, SEP IRAs, SIMPLE IRAs, Employer Sponsored ProfitSharing Plans, 401(k) Plans, 403(b) Plans and 457(b) Plans are all subject to an RMD. Your TPA should be able to help you with gathering all the information you need for the RMD, if they haven’g already done so.

Plan A Meeting With Your Investment Advisor.

It’s always smart to sit down with your investment advisor to review the investments in your fund. Checking up on your fund’s progress is part of the due diligence necessary for your plan. Remember to document the meeting and all the topics discussed. You should do a status review on the performance of the fund, which will help you decide if you need to make any changes. Are all of your files in compliance? Are the funds performing well? Do any funds need to be addressed or changed?

Review Your Plan’s Fidelity Bond.

This is an easy one. Your plan’s fidelity bond should be 10% of your plan’s assets.

Look Ahead.

Is their anyone who is about to become eligible to enroll in the plan? Did you hire anyone or fire anyone? Give your TPA a heads up.

You do year-end tax planning in December, and it’s the perfect time to do your year end retirement plan housekeeping. Taking a day to knock it out will not only ensure your plan is running smoothly, but also help prevent accusations of improper plan management. It’s all about covering your… bases.

This may seem like a lot to add to your plate, but your financial advisor and TPA are here to help you. It’s their job and they should be happy to do it. They have all the records and info you need to tackle this to-do list, so make the call and start checking items off now.

Remember it’ retirement we’re talking about. The more you know and understand, the better off you will be.

Best Regards,

President

MBA, QKA, CBC